GST legal heir procedure, When a registered taxpayer under GST passes away, their registration must be cancelled, and the business may be transferred to a legal heir. One of the key questions that often arises in such cases is — how to transfer the remaining balance in the Electronic Cash Ledger (ECL) of the deceased dealer to the GSTIN of the legal heir?

This article explains the complete procedure step-by-step, as per CBIC and GST law guidelines**.

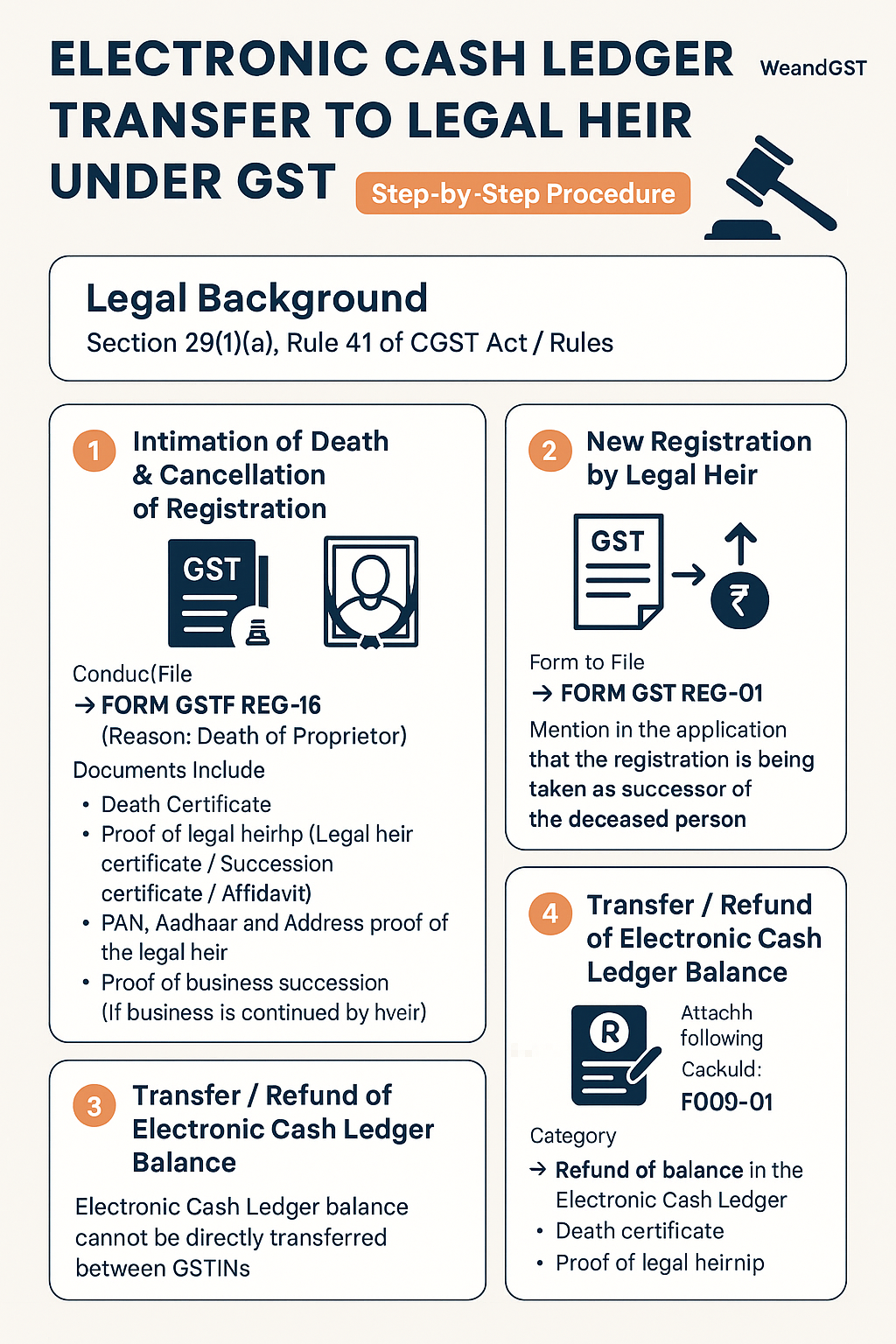

Legal Background⚖️

As per Section 29(1)(a) of the CGST Act, the registration of a person is liable to be cancelled when:

“the business has been discontinued, transferred fully, or otherwise disposed of.”

When a business is succeeded by a “legal heir”, “Rule 41 of the CGST Rules, 2017″ becomes applicable — this rule specifically deals with “transfer of business on account of succession”.

⚙️ Step-by-Step Procedure for Transfer / Refund

Step 1: Intimation of Death & Cancellation of Registration

The legal heir or representative must inform the jurisdictional GST officer about the death of the registered person and request cancellation of registration.

Form to File:

FORM GST REG-16 (Reason: Death of Proprietor)

**Documents Required:

* Death Certificate of the deceased taxpayer

* Proof of legal heirship (Legal heir certificate / Succession certificate / Affidavit)

* PAN, Aadhaar, and Address proof of the legal heir

* Proof of business succession (if business is continued by heir)

Step 2: New Registration by Legal Heir

The legal heir must obtain a new GST registration in their own name to continue the business.

Form to File

➡️ FORM GST REG-01

📌 Mention in the application that the registration is being taken as a successor of the deceased person.

Step 3: Transfer of Input Tax Credit (ITC)

If there is an Input Tax Credit balance in the deceased dealer’s account, it can be transferred to the new GSTIN.

Form to File

➡️ FORM GST ITC-02

Legal Reference:

Rule 41(1) of the CGST Rules, 2017 allows such transfer of ITC in case of business succession.

—

Step 4: Transfer / Refund of Electronic Cash Ledger Balance

The Electronic Cash Ledger (ECL) balance cannot be directly transferred between GSTINs.

Instead, the legal heir must apply for a refund of the remaining balance in the deceased’s cash ledger.

Form to File

➡️ FORM GST RFD-01**

Select Category

Refund of balance in the Electronic Cash Ledger

Attach the following documents:

* Death certificate

* Proof of legal heirship

* Copy of GST cancellation order of the deceased

* Proof of business succession / authorization

* Application letter requesting refund or transfer

Once approved, the refund amount is credited to the legal heir’s bank account. The heir can then deposit this amount into their own GSTIN’s cash ledger.

✅ Summary of Forms and Legal Provisions

| Step | Description | Form | Legal Provision |

| 1 | Cancellation due to death of proprietor | GST REG-16 | Sec 29(1)(a), Rule 20 |

| 2 | New registration by legal heir | GST REG-01 | Rule 8 |

| 3 | Transfer of ITC to new GSTIN | GST ITC-02 | Rule 41(1) |

| 4 | Refund of cash ledger balance | GST RFD-01 | Sec 54(1), Rule 92(1) |

💡 Important Notes

Direct transfer of the Electronic Cash Ledger balance between GSTINs is **not permitted**.

The refund process is the **only legally valid route**.

Jurisdictional GST officer may verify documents before approving the refund.

Always keep proper records of death, succession, and refund approvals for future reference.

🧩 Conclusion

If a registered dealer passes away, their Electronic Cash Ledger balance cannot be directly transferred to the legal heir’s GSTIN.

The legal heir must **first apply for refund** of the deceased person’s cash balance and then **deposit the amount** under the new registration.

This ensures smooth legal and tax compliance in cases of succession under GST.

-

GST legal heir procedure

-

GST succession transfer

-

Electronic Cash Ledger transfer

-

ECL refund deceased taxpayer

-

GST registration after death

-

GST cancellation due to death

-

GST ITC transfer to legal heir

-

GST refund RFD-01 deceased

-

GST REG-16 cancellation

-

Transfer of business under GST

-

GST death of proprietor compliance

-

How to transfer GST cash ledger balance

-

Refund of Electronic Cash Ledger

-

Legal heir GST process India

-

GST ITC-02 filing guide

-

GST cancellation documents required

-

Business succession under GST Rules

-

Section 29 CGST Act cancellation

-

Rule 41 CGST Rules ITC transfer

-

GST officer procedure on death

-

How to transfer GST balance from deceased person to legal heir

-

Steps for refund of Electronic Cash Ledger after death of proprietor

-

GST cancellation and new registration for legal heir

-

Documents required for GST succession and refund

-

Process for transferring ITC and ECL after proprietor’s death

-

GST refund for deceased dealer cash ledger balance

-

How legal heirs continue business under GST

#GST #LegalHeir #GSTSuccession #ElectronicCashLedger #GSTRefund

#GSTRegistration #GSTCompliance #SmallBusinessIndia #GSTITC #WeAndGST#GST #LegalHeir #ElectronicCashLedger #GSTRegistration #GSTRefund #GSTSuccession